The EC’s Proposed Industrial Carbon Management Strategy (2024-IP01)

Insight Papers

14 February 2024

On 6 February 2024, the European Commission (EC) released its highly anticipated Industrial Carbon Management Strategy. The European Union (EU) is committed to achieving economy-wide climate neutrality by 2050 to limit global warming to 1.5 °C.

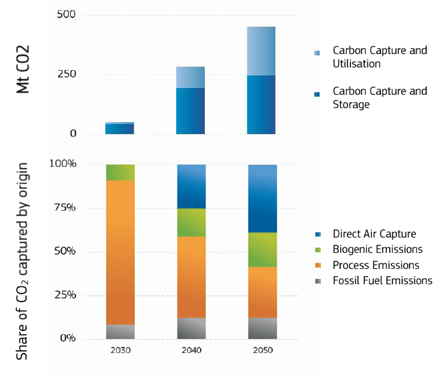

On 6 February 2024, the European Commission (EC) released its highly anticipated Industrial Carbon Management Strategy. The European Union (EU) is committed to achieving economy-wide climate neutrality by 2050 to limit global warming to 1.5 °C. It is implementing a comprehensive policy framework to reduce emissions by at least 55% by 2030 and the EC has now laid out the groundwork for the EU’s climate ambition for the next decade. This includes developing a common and comprehensive policy and investment framework for all aspects of industrial carbon management. The EU already has several policies in place to support the capture of CO₂. However, to reap its full economic potential in line with the ambition of the EU’s 2040 climate target Communication and to reach climate neutrality by 2050, the EU will need to significantly scale up efforts. In the Net Zero Industry Act (NZIA), the Commission has proposed that at least 50 MtCO₂/year can be stored geologically by 2030, 280 Mt would have to be captured by 2040 and around 450 Mt by 2050 (see Figure 1).

The scale of this challenge requires an EU-wide industrial carbon management strategy, which will be based on three pathways:

- Capturing CO₂ for storage (CCS): where CO₂ emissions of fossil, biogenic or atmospheric origin are captured and transported for permanent and safe geological storage.

- Removing CO₂ from the atmosphere (CDR): where permanent storage involves biogenic or atmospheric CO₂ and it will result in removing carbon from the atmosphere.

- Capturing CO₂ for utilisation (CCU): where industry uses captured CO₂ in synthetic products, chemicals or fuels. Whilst initially using all types of CO₂, over time a strategic focus of utilisation value chains on capturing biogenic or atmospheric CO₂ will yield higher climate benefits.

- CO₂ transport infrastructure is the key enabler common to all pathways.

Summary of key messages from the Communication

Deploying transport infrastructure for a single market for CO₂

- Develop a non-discriminatory, open-access, transparent, multimodal, cross-border CO₂ transport and storage infrastructure. The EC estimates that CO₂ transport networks, including pipelines and shipping routes, could cost up to EUR 12.2 billion in total by 2030, rising to around EUR 16 billion in total by 2040.

- Propose a possible future CO₂ transport regulatory package that will consider issues including market and cost structure, cross-border integration and planning, technical harmonisation and investment incentives for new infrastructure, third-party access, competent regulatory authorities, tariff regulation and ownership models.

- Propose an EU-wide CO₂ transport infrastructure planning mechanism in cooperation with Member States and the CCUS Forum stakeholder platform, including the reuse/repurposing of existing infrastructure.

- Nominate European coordinators to support the early development of (cross-border) infrastructure projects.

- Develop emissions accounting rules in the context of the EU ETS to enable all means of transport of CO₂ and ensure liability for leakage.

- Establish minimum standards for CO₂ streams to be used in a network code, applicable to all industrial carbon management solutions, and consider guidelines on ‘incidental associated substances’ to ensure the integrity of the infrastructure and reservoirs (and provide a balance between cost-effectiveness and risks).

- Promote through the International Maritime Organization (IMO) the development of any necessary guidelines on the safe transportation of CO₂ by sea.

Capturing and storing CO₂ emissions

- The ETS carbon price provides an incentive to capture CO₂ generated from fossil fuel and industrial process emissions. This incentive is expected to grow due to the last reform, as the ETS emissions cap is steadily decreasing further, setting a strong price expectation for carbon in the EU.

- Develop (by early 2026 at the latest) a platform for demand assessment and demand aggregation for CO₂ transport or storage services, to match CO₂ suppliers with storage and transport providers.

- Publish an investment atlas of potential CO₂ storage sites based on a common storage readiness level format.

- Use the knowledge-sharing platform for industrial CCUS projects to develop together with industry sectoral roadmaps for industrial carbon management.

- Develop (by 2025) step-by-step guidance for permitting processes for net-zero strategic projects for CO₂ storage, notably regarding:

- the transfer of responsibility from operators back to the competent authorities and the corresponding financial security and financial mechanism requirements;

- transparency on the permitting requirements and risk-based approaches to facilitate final investment decisions by storage operators.

- Member States should:

- include in their updated National Energy and Climate Plans their assessment of capture needs and storage capacity/options and identify actions to support the deployment of a CCS value chain.

- by 2025, ensure that they have transparent processes in place for storage permit applicants to engage with the competent authorities.

- support the development and rollout of cooperative net-zero strategic projects under the NZIA to create full carbon capture, transport and storage value chains, including across borders.

- by 2025 at the latest, enable their geological services to contribute existing data and to generate new data to contribute to an EEA-wide investment atlas of potential CO₂ storage sites.

Removing CO₂ from the atmosphere

- The EU could need carbon removals to balance out around 400 MtCO₂eq of residual emissions in hard-to-abate sectors.

- Industrial carbon removals are not currently covered by the EU ETS Directive nor the Effort Sharing or the Land, Land Use Change and Forestry (LULUCF) regulations. Since the EU ETS does not recognise negative emissions, capture and storage of biogenic and atmospheric CO₂ is not incentivised by the EU compliance carbon market price, and currently the only incentive at the EU level comes from the Innovation Fund. Investment decisions for this type of operation currently mainly rely on state subsidies or voluntary carbon markets. The forthcoming EU carbon removal certification framework will help mobilise financing while ensuring the environmental integrity of carbon removals but it is important that the EC assesses how best to provide incentives for industrial carbon removals in existing EU legislation or through new instruments.

- Assess overall objectives for carbon removal needs in line with the EU’s 2040 climate ambition and the goal to reach climate neutrality by 2050 and negative emissions thereafter.

- Develop policy options and support mechanisms for industrial carbon removals, including if and how to account for them in the EU ETS.

- Even if included under the EU ETS, for some types of removals, such as direct air carbon capture and storage (DACCS), the estimated future costs range from EUR 122 to EUR 539/tCO₂, well above the current ETS price. Integration in the EU ETS pricing system alone might thus be an insufficient incentive for industrial removals.

- Boost EU research, innovation and first-of-a-kind demonstration for novel industrial technologies to remove CO₂ under Horizon Europe and the Innovation Fund.

Using captured CO₂ as a resource to replace fossil fuels in industrial production

- CCU contributes to the circular economy model, which will gain further importance under the climate action framework up to 2040.

- Access to hydrogen is also needed to enable CCU technologies. Therefore, synergies between CCU applications and hydrogen networks can play a key role in boosting decarbonisation.

- Certain uses of captured CO₂ in products are supported by legislation. These rules encourage the deployment of CCU-based fuels to replace fossil fuels in key sectors, with safeguards in place to ensure that they provide the required minimum GHG emission savings (i.e. ETS Directive, ReFuelEU aviation, FuelEU Maritime Regulation). The use of such CCU fuels will also be recognised in the EU ETS to avoid double counting the embodied carbon emissions.

- The 2023 revision of the EU ETS Directive also acknowledges the permanence of carbon storage in certain types of products. The EC is preparing a delegated act to specify the conditions under which permanent storage can be recognised, to put permanent CCU and CCS on an equal footing in the ETS. The EU carbon removal certification framework will give the option to certify carbon removals generated by industrial activities storing atmospheric or biogenic carbon in products in a manner that prevents the carbon from being re-emitted to the atmosphere.

- The Sustainable Carbon Cycles Communication also set the objective of achieving 20% of the carbon used in chemical and plastic products originating from sustainable non-fossil sources by 2030.

- Assess demand pull options to increase the uptake of sustainable carbon as a resource in industrial sectors in full consideration of the EC’s upcoming Biotech and Biomanufacturing initiative.

- Use the knowledge-sharing platform for industrial CCUS projects to co-develop with industries sector-specific roadmaps on CCU activities.

- Draw up a coherent framework to account for all industrial carbon management activities that accurately reflect the climate benefits across their value chains, and to incentivise the deployment of innovative and sustainable permanent and non-permanent CCU applications.

Investing and funding the clean carbon transition

- The proposed NZIA target of 50 Mt of annual CO₂ storage capacity by 2030 requires approximately EUR 3 billion investments in carbon storage facilities. Furthermore, estimated investment needs for the transport infrastructure of pipelines and ships associated with the NZIA target are between about EUR 6.2 and 9.2 billion by 2030. The capture costs from point sources are estimated to range from EUR 13 and EUR 103/tCO₂. However, estimated funding shortfalls are cumulatively EUR 10 billion by 2030 for currently announced CCS projects. Beyond 2030, the EC estimates that the required investment needs in CO₂ transport infrastructure would rise to between EUR 9.3 and 23.1 billion in 2050 to meet the 2040 and 2050 objectives. Despite increasing investment needs, a commercially viable market is expected to begin to take shape after 2030, where investors can earn a competitive return on invested capital based on the EU carbon price. Thus, the carbon price signal in the EU ETS will be key to making CCS projects commercially viable. Ultimately, these investment needs are set against an estimated extrapolated theoretical market potential of captured CO₂ in the EU of between 360 and 790 MtCO₂, which could generate between EUR 45 billion and EUR 100 billion in the total economic value of the future CO₂ value chain in the EU from 2030 onwards and help create between 75 000 and 170 000 jobs.

- Transparent and coordinated design of a possible important project of common European interest for CO₂ transport and storage infrastructure via the Joint European Forum for Important Projects of Common European Interest (JEF-IPCEI). To start the process as soon as possible, use the existing CCUS Forum platform.

- Assess by 2025 whether certain CO₂ capture installations, such as cement or lime production facilities, are mature enough and sufficient competition may be expected to move from project-based grant support to market-based funding mechanisms, such as competitive bidding auctions as a service under the Innovation Fund.

- A first competitive bidding mechanism is being pioneered under the Innovation Fund’s pilot auction for renewable hydrogen production in the EU.

- Engage with the European Investment Bank (EIB) on financing of CCS and CCU projects.

- Facilitate investment needs in industrial carbon management up to 2040 and 2050, including by making smart use of public funding to leverage private investment.

Public awareness

- It is essential that Member States stimulate and support an inclusive, scientifically informed and transparent debate on all industrial carbon management technologies. Moreover, ensuring social, environmental, and health safeguards will be key in supporting responsible implementation and public adherence.

- The EC will use the CCUS Forum and other Commission fora, including the European Sustainable Energy Week, to stimulate public debate and increase public understanding and awareness.

- The EC will also monitor public opinion on industrial carbon management, including through Eurobarometer surveys, and it will encourage Member States to measure public awareness at a national level.

- Work with Member States to specify operating conditions for CO₂ transport and storage projects that can reward local communities for hosting them.

- Work with Member States and industry to increase knowledge, awareness and public debate on industrial carbon management.

Research and innovation

- During the period 2007-2023, the EC has invested more than EUR 540 million in innovative CCUS solutions through its successive framework programmes for research and innovation (FP7, Horizon 2020 and Horizon Europe).

- Access to readily available and open data is needed for research to support components for standardisation and help avoid overly strict limitations.

- Support a new collaboration and knowledge-sharing platform for industrial CCUS projects.

- Continue to invest in R&I for industrial carbon management technologies, including energy and cost efficiency optimisation of processes and pre-normative research to contribute to standardisation.

Cross-border and international cooperation

- The first commercial cross-border agreement to capture CO₂ produced in the EU and ship it for storage in Norway has already been signed. For Member States of the European Economic Area (EEA), the implemented EU legal framework is the relevant ‘arrangement’ between the Parties in the meaning of Article 6(2) of the international 1996 Protocol to the Convention on the Prevention of Maritime Pollution by Dumping of Waste and Other Matter, 1972 (the ‘London protocol’). Accordingly, any operator of CO₂ transport networks and/or CO₂ storage sites can draw the full benefit of the EU’s legal framework to import or export captured CO₂ within the EEA.

- For the time being, the only way to extend such benefits to non-EEA countries would be to operate storage sites under an ETS linked with the EEA ETS and under a framework that provides legal safeguards equivalent to the EU’s CCS Directive.

- Work towards accelerated international cooperation to promote harmonised reporting and accounting of industrial carbon management activities, to ensure they are accurately accounted for under the UNFCCC transparency framework.

- Work to ensure that international carbon pricing frameworks focus on the necessary emissions cuts while providing for carbon removals to tackle emissions in the hard-to-abate sectors.

- IEAGHG comments and conclusions:

- IEAGHG is active in all the pathways and enabling areas crucial for this strategy and will continue to support the EU and our members in delivering this important and necessary strategy.

References

The Communication can be found here:

https://energy.ec.europa.eu/document/download/6b89e732-fea4-480b-9d2e-cf64de90247e_en?filename=Communication_-_Industrial_Carbon_Management.pdf

Other articles you might be interested in

Get the latest CCS news and insights

Get essential news and updates from the CCS sector and the IEAGHG by email.

Can't find what you are looking for?

Whatever you would like to know, our dedicated team of experts is here to help you. Just drop us an email and we will get back to you as soon as we can.

Contact Us Now